Making Sense of the Details Behind Your Financial Records

Introduction

Many business owners review their profit and loss statements and balance sheets but rarely look at the information that creates those reports. Behind every financial statement is a collection of general ledger entries that record the day-to-day financial activity of the business.

Understanding general ledger entries can help you identify errors, monitor spending, detect fraud, and make better financial decisions. You do not need an accounting degree to understand the basics. Knowing what to look for can give you greater confidence in your financial records and help you stay informed about your company’s financial health.

In this article, we will explain what general ledger entries are, why they matter, and what business owners should pay attention to when reviewing them.

What Is a General Ledger?

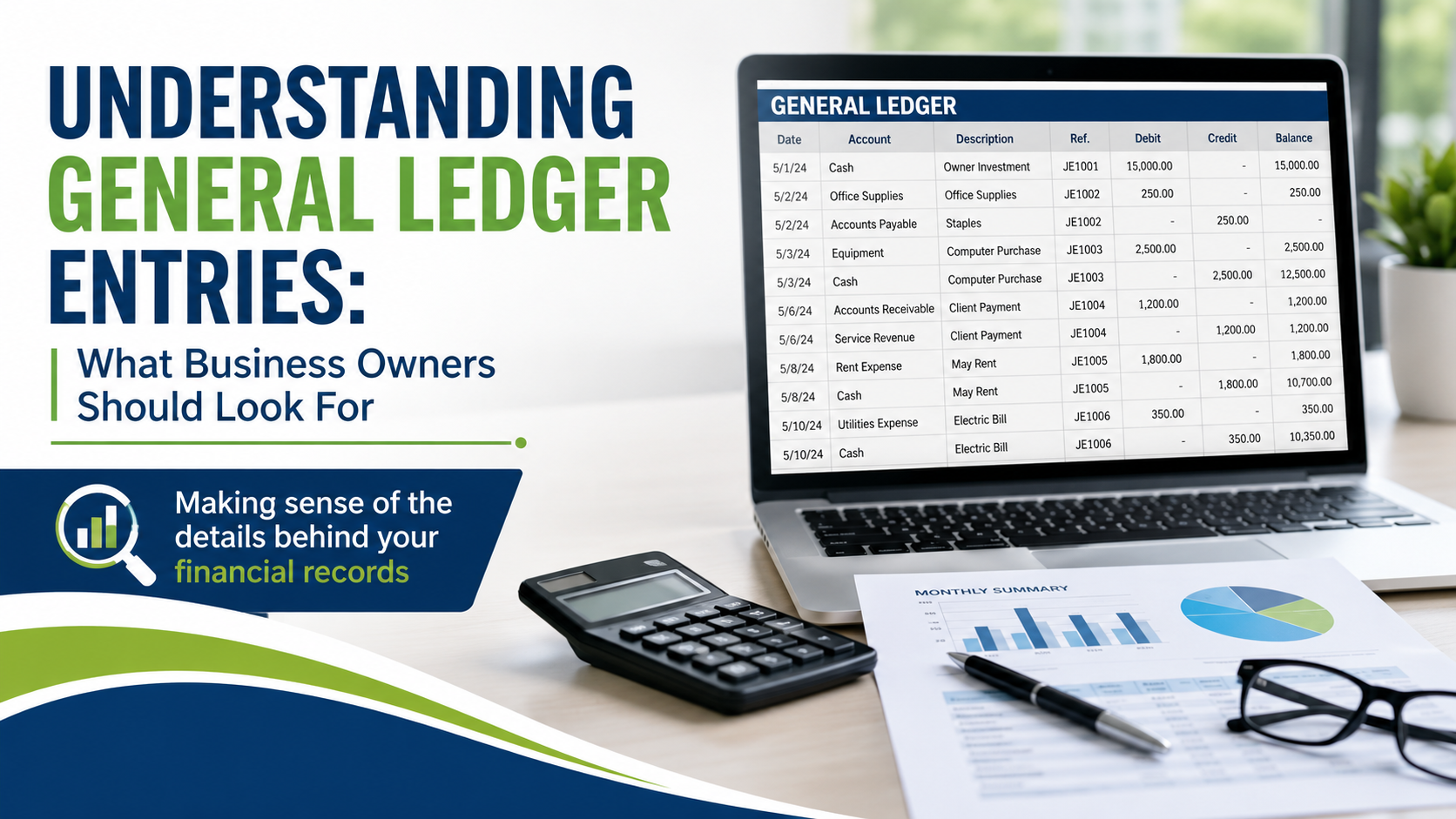

A general ledger is the central record-keeping system for your business finances. It contains all financial transactions organized by account.

Every transaction recorded in your accounting system eventually flows into the general ledger, including:

- Sales revenue

- Customer payments

- Vendor bills

- Expense payments

- Payroll transactions

- Loan payments

- Asset purchases

- Sales tax transactions

The general ledger serves as the foundation for your financial statements.

Think of it as the detailed history behind the numbers shown on your profit and loss statement and balance sheet.

What Is a General Ledger Entry?

A general ledger entry records a financial transaction in your accounting system.

Each entry typically includes:

- Transaction date

- Account names

- Debit amount

- Credit amount

- Description or memo

- Reference number

For example, if a business pays a utility bill of $500, the entry might look like this:

| Account | Debit | Credit |

|---|---|---|

| Utilities Expense | $500 | |

| Cash | $500 |

This entry shows that utility expenses increased while cash decreased.

Why Business Owners Should Review Ledger Entries

Many business owners rely solely on monthly reports prepared by their bookkeeper or accountant. While those reports are important, reviewing ledger details can help uncover issues that summary reports may not reveal.

Benefits include:

- Catching bookkeeping errors early

- Identifying duplicate transactions

- Monitoring employee spending

- Detecting unusual activity

- Improving budgeting decisions

- Supporting tax preparation

- Ensuring accurate financial reporting

Even a quick review each month can help prevent costly mistakes.

Key Information to Review in General Ledger Entries

1. Transaction Descriptions

One of the first things to review is the description attached to each transaction.

Descriptions should clearly explain:

- What was purchased

- Who was paid

- Why the transaction occurred

For example:

Good description:

- Office supplies purchased from Staples

Poor description:

- Expense

Clear descriptions make it easier to understand spending patterns and answer questions during tax season.

2. Account Classifications

Transactions should be posted to the correct accounts.

Common expense categories include:

- Advertising

- Office supplies

- Rent

- Utilities

- Payroll

- Professional services

- Vehicle expenses

Misclassified transactions can distort financial reports.

Example

If a new computer costing $2,500 is recorded as office supplies instead of a fixed asset, expenses may appear higher than they should be while assets are understated.

Proper classification helps ensure accurate reporting and tax compliance.

3. Unusual or Unexpected Transactions

Business owners should periodically scan for transactions that seem unusual.

Watch for:

- Large purchases

- Unexpected vendor payments

- Duplicate charges

- Transactions outside normal business activity

- Payments to unfamiliar vendors

Example

If your average monthly software expenses are $300 and you notice a $3,000 software charge, that entry deserves investigation.

Unusual transactions are not always errors, but they should be understood and documented.

4. Duplicate Entries

Duplicate transactions are one of the most common bookkeeping mistakes.

Duplicates can occur when:

- Bills are entered twice

- Bank feeds import transactions incorrectly

- Multiple employees enter the same expense

Example

A $750 vendor payment accidentally recorded twice increases expenses by $750 and understates cash by the same amount.

Regular ledger reviews can help identify these issues before month-end reports are finalized.

5. Journal Entries Without Clear Documentation

Journal entries are adjustments made directly in the accounting system.

While they are often necessary, they should always include supporting documentation and explanations.

Business owners should ask questions when they see:

- Large adjusting entries

- Entries with vague descriptions

- Entries without supporting records

A properly documented journal entry provides transparency and supports financial accuracy.

6. Payroll Transactions

Payroll is often one of the largest business expenses.

Review payroll-related ledger entries for:

- Gross wages

- Payroll tax expenses

- Employer tax liabilities

- Benefits expenses

Make sure payroll amounts align with expectations and employee records.

Unexpected increases may indicate:

- Data entry errors

- Incorrect tax calculations

- Unauthorized payroll changes

7. Accounts Receivable Activity

The ledger can provide valuable insight into customer payment activity.

Look for:

- Large outstanding balances

- Customer credits

- Write-offs

- Adjustments

Example

If a customer with a history of timely payments suddenly has an overdue balance, you may need to follow up before the account becomes difficult to collect.

Strong accounts receivable management supports healthy cash flow.

8. Accounts Payable Activity

Reviewing vendor-related entries can help manage cash flow and avoid missed payments.

Watch for:

- Overdue vendor balances

- Duplicate bills

- Unusual payment amounts

- Vendor credits

Maintaining accurate accounts payable records helps preserve vendor relationships and avoid unnecessary penalties or late fees.

Red Flags Business Owners Should Never Ignore

Certain ledger entries deserve immediate attention.

Frequent Negative Cash Balances

Repeated negative balances may indicate:

- Cash flow problems

- Timing issues

- Recording errors

Large Round-Dollar Transactions

Entries such as:

- $5,000

- $10,000

- $25,000

are not necessarily wrong, but they often warrant additional review.

Excessive Adjustments

Too many adjusting entries may suggest bookkeeping processes need improvement.

Missing Supporting Documents

Every significant transaction should have documentation such as:

- Invoices

- Receipts

- Contracts

- Bank records

Missing documentation can create challenges during audits and tax preparation.

How Often Should You Review Your General Ledger?

For most small businesses, a monthly review is a good practice.

A monthly review should include:

- Reviewing major expenses

- Checking account balances

- Looking for unusual transactions

- Confirming payroll activity

- Verifying customer and vendor balances

Businesses with higher transaction volumes may benefit from weekly reviews.

Tips for Making Ledger Reviews Easier

Use Consistent Account Names

Consistent account structures improve reporting accuracy and simplify reviews.

Attach Supporting Documents

Store invoices, receipts, and contracts directly within your accounting software whenever possible.

Reconcile Accounts Monthly

Bank and credit card reconciliations help ensure ledger entries match actual financial activity.

Work With a Professional Bookkeeper

A qualified bookkeeping professional can help maintain accurate records, identify issues early, and provide meaningful financial insights.

Conclusion

The general ledger is much more than an accounting record. It is a valuable tool that helps business owners understand what is happening behind their financial statements.

By reviewing general ledger entries regularly, you can identify errors, monitor spending, improve cash flow management, and make more informed business decisions.

You do not need to examine every transaction every day. However, taking time each month to review key entries, account balances, and unusual activity can help ensure your financial records remain accurate and reliable.

For business owners who want a clearer picture of their finances, understanding the general ledger is an excellent place to start..

How Accredited Bookkeeping Can Support Your Business

At Accredited Bookkeeping, we understand the challenges small businesses face when it comes to managing finances. We’re here to help you streamline your bookkeeping processes, avoid unnecessary financial errors, and gain greater clarity about your financial health. Our services are designed to fit the specific needs of your business, giving you peace of mind while you focus on growth.

Contact us today for a free consultation and discover how we can make bookkeeping easier for you.

marianne@accreditedbookkeeping.com

marianne@accreditedbookkeeping.com

Marianne Kirwan

352-626-0116

352-626-0116 Schedule a meeting

Schedule a meeting