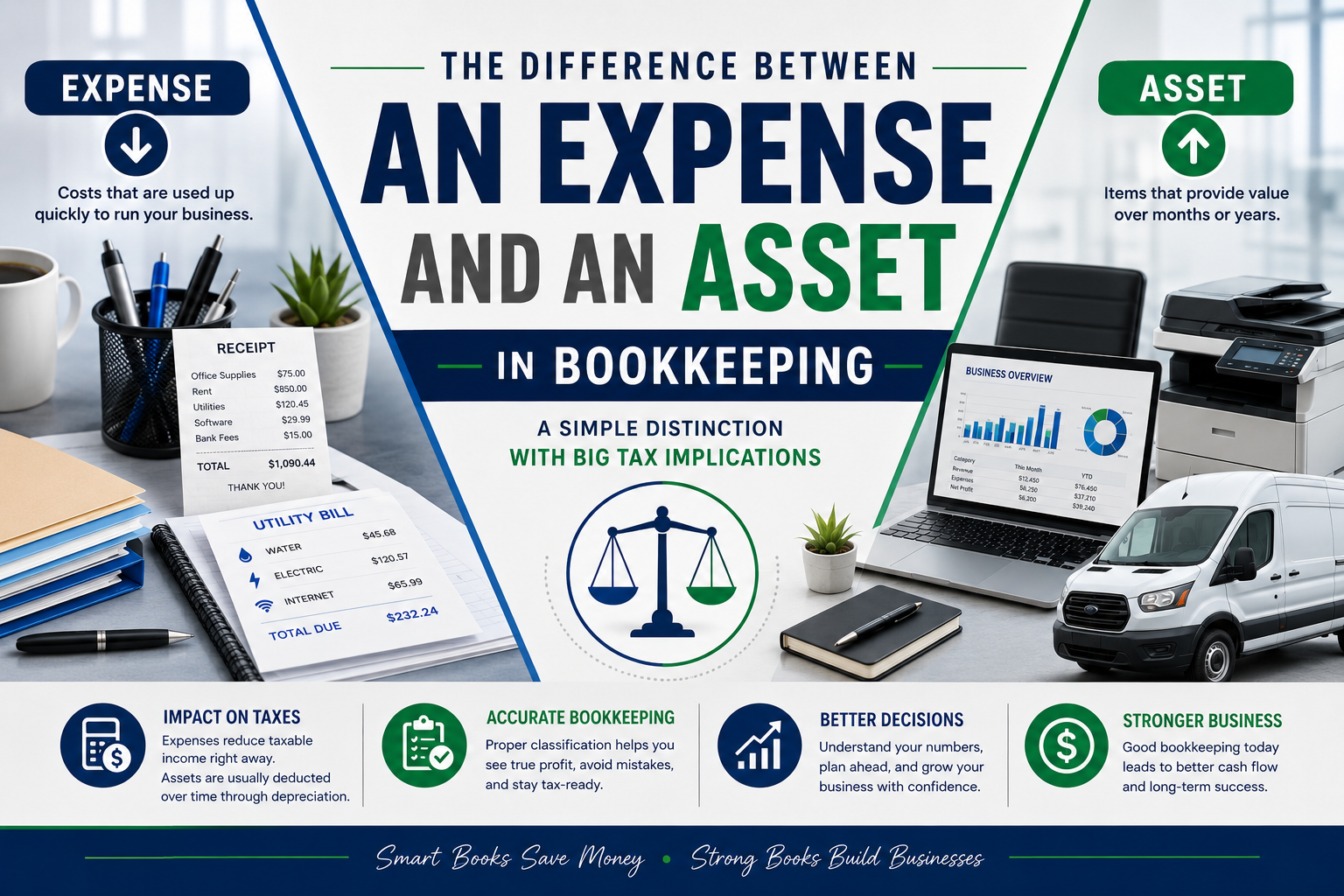

A simple distinction with big tax implications

For small business owners, the difference between an expense and an asset may seem like a bookkeeping detail. But this simple distinction can affect your tax deductions, profit reports, cash flow planning, and long-term financial decisions.

What Is an Expense?

An expense is a cost your business pays to operate day to day. It is usually used up quickly and helps your business run in the current period.

Common examples include:

- Office supplies

- Rent

- Utilities

- Advertising

- Software subscriptions

- Bank fees

- Repairs and maintenance

- Professional services

In general, deductible business expenses must be both ordinary and necessary, meaning they are common in your industry and helpful for your business.

What Is an Asset?

An asset is something your business owns that provides value over time. Instead of being used up right away, it helps the business for months or years.

Common examples include:

- Computers

- Equipment

- Vehicles

- Furniture

- Machinery

- Buildings

- Certain software

- Large improvements to property

Assets are usually recorded on the balance sheet, not deducted all at once as a regular expense.

The Simple Rule

Ask this question:

Will this purchase help the business for more than one year?

If yes, it may be an asset.

If no, it is more likely an expense.

For example, printer paper is an expense because it gets used up quickly. A $2,000 laptop is usually an asset because it will likely be used for several years.

Why This Matters for Taxes

Expenses often reduce taxable income right away. Assets are usually deducted over time through depreciation, which means spreading the cost across the asset’s useful life.

However, tax rules may allow some assets to be deducted faster. For 2025, the IRS lists a maximum Section 179 deduction of $2,500,000, subject to limits and eligibility rules.

That does not mean every asset should automatically be written off immediately. The right choice depends on your income, cash flow, tax situation, and future plans.

Expense vs. Asset Examples

Example 1: Office Supplies

A Florida consultant buys $75 of pens, folders, and notebooks.

That is likely an expense because the items are small, routine, and used quickly.

Example 2: Laptop

A freelance designer buys a $1,800 laptop used mainly for client work.

That is likely an asset because it will help the business for more than one year.

Example 3: Repair vs. Improvement

A restaurant pays $300 to fix a broken refrigerator part.

That may be a repair expense.

But if the restaurant buys a new commercial refrigerator for $6,000, that is likely an asset.

Bookkeeping Impact

Classifying purchases correctly helps you understand your real profit.

If you record a large asset as an expense, your profit may look too low. If you record an expense as an asset, your profit may look too high. Either mistake can lead to poor decisions, tax issues, or messy financial reports.

Practical Tips for Small Business Owners

- Keep receipts for all major purchases. Include what was bought, when, and how it is used.

- Separate small supplies from larger equipment.

- Ask whether the item will last more than one year.

- Track business use percentage, especially for vehicles, phones, and computers.

- Review large purchases before tax time, not after.

Conclusion

The difference between an expense and an asset is simple but important. Expenses usually support daily operations and may be deducted right away. Assets provide long-term value and may need to be depreciated or handled under special tax rules.

Accurate bookkeeping helps small business owners see the full picture, avoid confusion, and make better financial decisions throughout the year.

How Accredited Bookkeeping Can Support Your Business

At Accredited Bookkeeping, we understand the challenges small businesses face when it comes to managing finances. We’re here to help you streamline your bookkeeping processes, avoid unnecessary financial errors, and gain greater clarity about your financial health. Our services are designed to fit the specific needs of your business, giving you peace of mind while you focus on growth.

Contact us today for a free consultation and discover how we can make bookkeeping easier for you.

marianne@accreditedbookkeeping.com

Marianne Kirwan

352-626-0116